Why Is Your Portfolio Invested the Way it Is?

By Russell Holcombe, MTx, CFP®

I wake up early by most standards, a ludicrous hour for those that enjoy sleep. For me, reading is best done early, and these days I find it more interesting than ever. Absorbing stories about the financial straightjacket that the Fed now has to get out of. At least Houdini knew the way out before he jumped in the tank. Only the audience was left to wonder how he would survive.

As I listened to the financial pundits on CNBC at 5:00 a.m. recently, a financial advisor shared a story about a interaction with a prospect concerning her portfolio. My eyes quickly left the book I was reading to focus on what the expert had to say. The confused prospect had said, “I thought my bonds were supposed to protect me when markets declined. Why are they down 10%? What should I do next?” The prospect’s first introduction to the risk of bond investing had landed in the form of a brokerage statement in her mailbox. The expert’s response left me floored: “Do nothing. You have already taken the loss so there’s nothing to do.” Nothing to do?! Her potential client got bad portfolio advice from someone that didn’t understand bond risk and the expert’s response was to do nothing. I returned to my book disgusted.

It has been 40 years since the bond bull market began, and memories of the portfolio damage caused by rising interest rates are stories only history books can tell. Sadly, the sages of history are not around to share with us their experience during the Great Depression or inflation and supply chain disruptions caused by the events leading up to World War II.

Why was the woman surprised when she opened her statement? She was probably told her bond portfolio was supposed to protect her, but it did not hold up during a market decline. Her diversification didn’t work. Her advisor didn’t understand. She was taking a risk she knew nothing about, and she was now begging for someone to help her understand. Again the advice gave no hope.

I write this piece to help people get reacquainted with the risk of bond investing. (It is not volatility as the academics and financial advisors like to preach.) Theone asset class that can upend any portfolio—bonds.

Bonds exist in a portfolio to lessen the drawdown risk during market declines. Drawdown is defined as the amount of loss one would incur in a market decline. Most people are prepared for a 20% loss, but few have the stomach for a 40-50% loss. Bonds are there to protect your portfolio. The two primary ways to lose money in bonds: rising interest rates and defaults.

Rising Interest Rates

As stated earlier, we have been in a 40-year bull market in bonds. The Fed tested 0% interest rates, and it didn’t take long to figure out inflation is a really ugly side effect. Supporting demand when supply is constrained is a nasty combination.

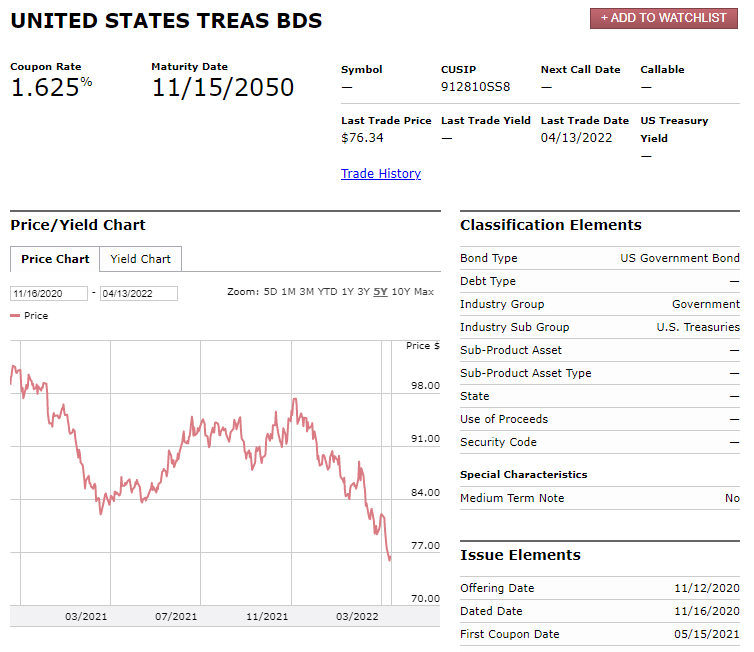

For the unwary bond investor, the damage has been particularly severe and is probably best illustrated with a real-world example. In November 2020 at the epicenter of interest rate suppression, the U.S. Treasury issued the following 30-year bond at 1.625% coupon. An investor with $100,000 invested would earn $1,625 per year for the next 30 years, and in 30 years, the investor will get their $100,000 back. As rates have risen, new 30-year Treasuries are yielding 2.875%. A “safe” bond purchased less than two years ago lost almost 25% of its value, as shown in the chart below. The Barclays iShares U.S. Aggregate Bond Index, which is a staple in most institutionally designed portfolio allocations, lost over 12% over the same time. By contrast, the S&P 500 gained just over 6%. (1)

Default

The other important thing to remember with bonds is there is no upside; you will get back exactly the same amount you loaned. No matter how strong the company, no matter how much their earnings rise, the bond’s only potential is to return exactly what you lent the company plus interest. Nothing more. You have very little to gain and a lot to lose. As Benjamin Graham and David Dodd stated in their 1934 Security Analysis, “Since the chief emphasis must be placed on avoidance of loss, bond selection is primarily a negative art.” The co-authors wrote, “It is a process of exclusion and rejection, rather than of search and acceptance.”

The Fed suppression of interest rates and record stimulus has allowed companies to live when they likely should have died. As of February 2022, the U.S. high-yield default rate over the last 12-month default volume barely registers at 0.3%. In the history of the index, it has never been this low. The last two years have experienced the lowest default rate in recorded history. When rates rise, it will likely trigger a return to normal default rates. Since there is no upside on bonds, investors in corporate and especially high-yield corporate bonds are probably not going to be pleased with the results if they are over-exposed to bonds rated BBB or lower.

Post Mortem

If I could review the bond portfolio of the prospect mentioned above, I probably would find two things: her maturity was too long for a rising interest rate environment, and her exposure to default risk was too high. She was not prepared for either and needed to make some changes. And unlike the advice from the so-called expert, there is never a bad time to fix a broken portfolio.

Is your portfolio at risk? Are you unsure if you have the right allocation? Holcombe Financial fixes broken portfolios. Sign up for a free 30-minute portfolio review by calling us at (404) 257-3317 or emailing hello@holcombefinancial.com.

About Russell

Russell (Rusty) Holcombe is the CEO and strategist at Holcombe Financial, a financial advisory firm serving entrepreneurs and corporate executives and managers. With over 25 years of experience, Rusty spends his days leading Holcombe Financial (a firm his father founded) and providing financial services that help his clients grow and protect their wealth so they can experience financial independence. Rusty is the author of You Should Only Have to Get Rich Once, which has won multiple awards, and created Holcombe Financial’s proprietary financial planning software, which helps clients make smarter financial decisions.

Rusty earned a bachelor’s degree in business administration with a focus in finance and real estate from Southern Methodist University and a master’s degree in taxation from Georgia State University. He is also a CERTIFIED FINANCIAL PLANNER™ professional. In his free time, Rusty and his wife, Regina, tend to their personal farm and grow their own food. You can often find him pursuing his hobby of long-distance running. To learn more about Rusty, connect with him on LinkedIn. You can also watch his latest webinar on investing.

______________

(1) Factset